The prospect of a motor insurance revolution is a hot topic and there is currently much discussion around how technology is finally transforming the industry. But it’s not just motor insurance companies themselves that are part of the revolution, as other major players discover that by using their GPS data for risk analysis, they become part of the next generation of motor insurance influencers and providers.

The motor insurance industry has started to evolve. Less of a revolution, more of an evolution. And a gradual development is more in line with an industry that, in many ways, is a very traditional one. There are many reasons why the industry needs to evolve. One is that many insurers are sitting on heavy legacy systems that they don’t know how to change. Another is that, as I’ve discussed previously, the industry is based on traditional risk proxies. The proxy system is unfair on customers and ultimately bad for profitability. The minute you use technology to avoid using proxies, the more satisfied the customer will be. And the more profitable the insurer will become.

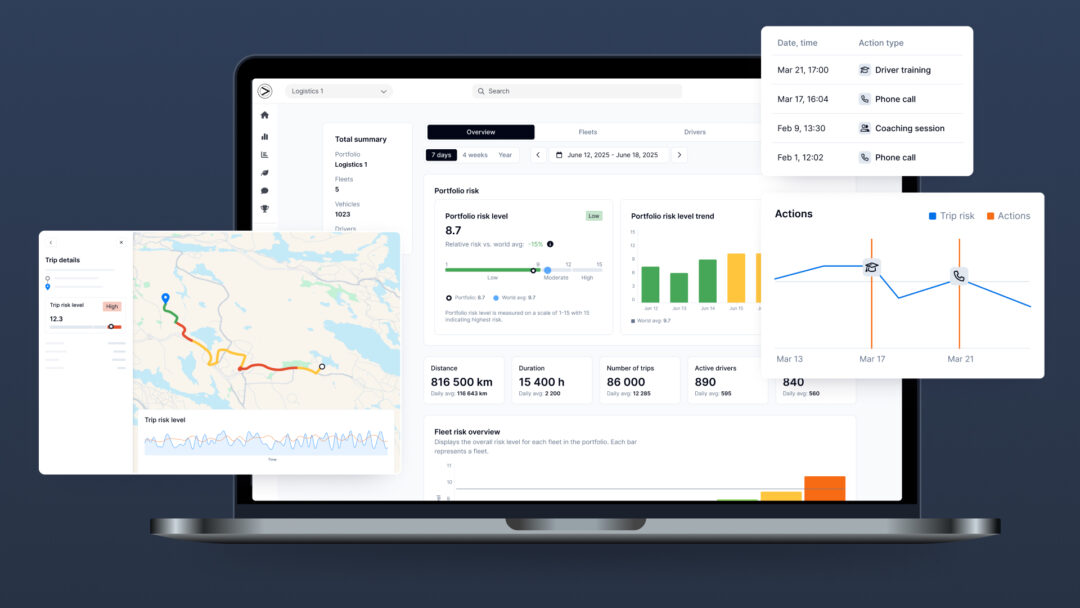

Some insurers have already introduced telematics to include an element of mobile risk-based pricing in their offerings. However, traditional telematics solutions can have drawbacks including cost, the potential for false negatives and frictional proxy-based propositions causing disaffection between drivers and suppliers.

Today’s world moves differently compared with even just a few years ago. This raises the question of how relevant traditional motor insurance propositions are in the current market. The COVID-19 pandemic has resulted in many people working from home at least part of the time. This means that people’s cars are also sitting at home. Motor insurers should therefore be asking themselves how to compensate drivers on the days they don’t use their cars and therefore aren’t at risk. Similarly, how to compensate drivers who use less busy and therefore safer roads and also display safer driving behaviors.

As the global focus on sustainability increases in coming years, it will become more important for insurance companies to really investigate the ecology of vehicle use. Therefore, it’s not only about compensating customers for lower risk, but rewarding them for creating fewer CO2 emissions. Technology enables insurance companies to construct risk-based, sustainable propositions very quickly without changing their legacy systems. But they’re not the only ones identifying opportunities in the market.

An understanding of the customer is at the core of the insurance revolution. And the latest AI technology makes it possible for any company with GPS data to gain that understanding. This starts by identifying the 15% of drivers causing 50% of crashes and the 85% of drivers who are lowest risk. And it completely overturns traditional driver risk analysis methods. More importantly, it has opened doors to new players in insurance.

Let’s think about telematics service providers (TSPs), who already sit on vast amounts of driver data. By using AI technology to uncover new layers of risk knowledge about their customer base, TSPs are ideally placed to launched new, behavior-based insurance products. Fleets can be in a similar position. Those with comprehensive driver risk management programs that use AI to determine a risk profile for each driver are ideally placed to partner with insurers in offering tailored products. And we must not forget the automotive makers, with GPS from connected car activity.

An important point to consider is that, for many traditional insurance companies today, the only contact they have with many of their customers is once per year, at renewal time. Why? Primarily because neither of them have anything to say! The companies that transform this relationship are the ones really owning the insurance revolution.

Anyone using GPS data can monetize their data. By accessing additional layers of information about the drivers in their customer base to understand crash probability, any company – traditional insurer, TSP, fleet, mobility provider or automotive – can understand driver risk and associated cost. This positions them perfectly to grasp a piece of the motor insurance market and revolutionize the way the industry operates.

Greater Than’s AI empowers any user of GPS data with more decision-making power than ever before. It converts existing GPS data into DriverDNA profiles that predict crash risk, associated cost, and sustainability impact. Contact Greater Than or book a meeting with me to discover more.