New in-depth insight into existing customers and an extensive loyalty program on top of a current portfolio is a good start for getting ready for the new sharing economy and user-based insurance. But is it that simple?

What sounds like a smooth transition is one of the biggest challenges today’s insurers are facing. Simply put, the math that weighs the cost of potential risks against the value of rewarding good behavior is challenging. Add to that the fear of not being able to recover already lost money at the ever-increasing receivables costs.

Don’t we recognize this? Isn’t what every industry is facing in shifts? Old business models are being replaced. User behavior is in focus. I’m thinking of, in the example, the great transition the whole mobile phone industry went through. Before and after apps.

Car insurance today is based on monthly payment and deductible—cost based on traditional statistics, where the vast majority also pays for the riskiest policyholders. As a result, most policyholders are likely to choose the insurance that covers them the most and costs them the least—the cheapest in short. And with no incentive whatsoever to behave well, drive safer or even to remain loyal as a customer.

But if there were benefits or anything else that allowed one to affect the individual costs personally.

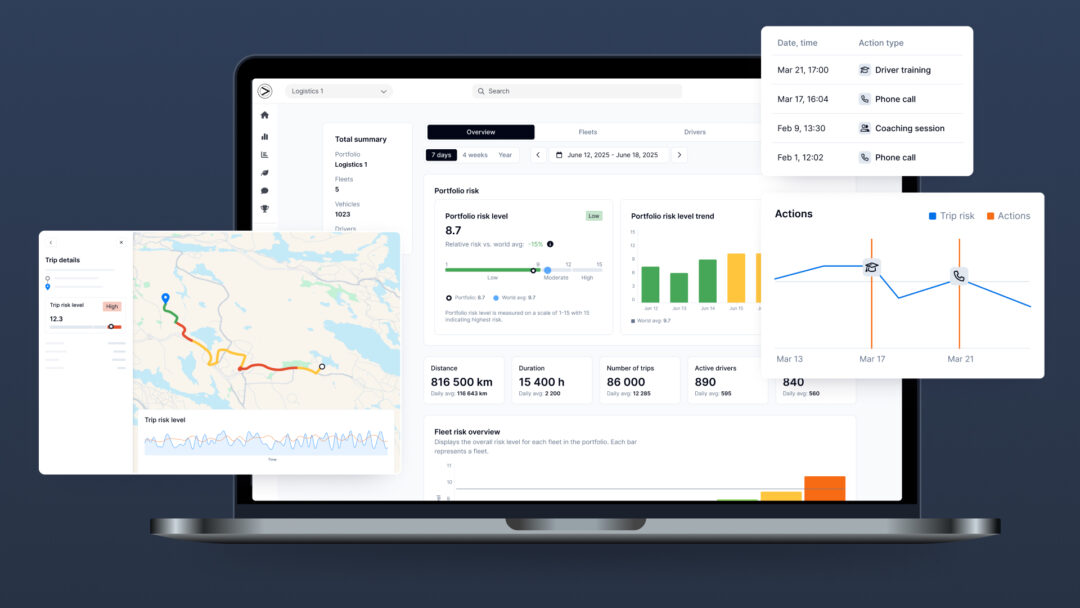

The basis for this is what we call UBI – user-based insurances – Insurance policies that are personalized with perks and benefits. Based on an individual’s usage and behavior with personal treats. This, at no surprise, is also one of the most potent triggers to promote better driving behavior and strong loyalty. We know some about this.

End-users using our UBI solutions improve their driving behavior and dramatically reduce their energy consumption – in less than a month. The number of accidents decreases by up to 50% and fuel consumption by 15-25%. A little more surprisingly, we have also learned that drivers with services like ours continuously increase their safe and energy-efficient driving style on the road—all for the better for the environment, people, and road safety in general.

We also know that just by adding real-time analysis of risk and its insights to an existing portfolio, dramatically changes how risks are perceived and identified within an organization. It’s quite often a door opener to new and updated ways to build new business models.

But what comes first – the hen or the egg? Real game-changers like, in the example of, Spotify, Apple, and Uber, did put the end-user in focus from day one. Which other industries dare to do the same? One thing is for sure; the end-user focus is the next deal-breaker for the game.